Swaps

•Download as PPT, PDF•

0 likes•911 views

An interest rate swap involves the exchange of interest payment streams between two parties, where one pays a fixed rate of interest and receives a floating rate, and vice versa. It allows parties to hedge against interest rate risk and borrow at more advantageous rates. A coupon swap specifically refers to an interest rate swap where only the interest payments are exchanged and not the principal. It provides benefits to both parties by allowing each to borrow at a lower rate in their preferred market.

Report

Share

Swaps

- 1. swapsswaps -- swap means exchange-- swap means exchange -- exchange of future cash flows between two-- exchange of future cash flows between two parties on a predetermined basisparties on a predetermined basis -- a nseries of forward contracts-- a nseries of forward contracts -- types-- types I Interest rate swapI Interest rate swap -- coupon swap-- coupon swap -- basis swap-- basis swap -- cross – currency swap-- cross – currency swap

- 2. COUPON SWAP A FLOWCOUPON SWAP A FLOW CHARTCHART Abc requires 7 year fixed rate funding Abc raises a 7 year floating rate debt at 0.50% over libor (i.e. in the market where it has a comparative advantage) Abc locatesxyz , a company which needs 7 year floating rate funds

- 3. Interest rate swapsInterest rate swaps Coupon swapCoupon swap OrOr Plain vanilla coupon swapPlain vanilla coupon swap

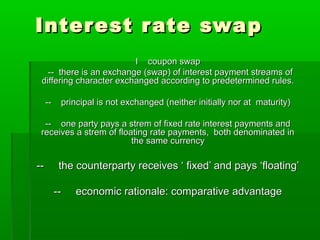

- 4. Interest rate swapInterest rate swap I coupon swapI coupon swap -- there is an exchange (swap) of interest payment streams of-- there is an exchange (swap) of interest payment streams of differing character exchanged according to predetermined rules.differing character exchanged according to predetermined rules. -- principal is not exchanged (neither initially nor at maturity)-- principal is not exchanged (neither initially nor at maturity) -- one party pays a strem of fixed rate interest payments and-- one party pays a strem of fixed rate interest payments and receives a strem of floating rate payments, both denominated inreceives a strem of floating rate payments, both denominated in the same currencythe same currency -- the counterparty receives ‘ fixed’ and pays ‘floating’-- the counterparty receives ‘ fixed’ and pays ‘floating’ -- economic rationale: comparative advantage-- economic rationale: comparative advantage

- 5. Some companies have a comparative advantage in the fixed rateSome companies have a comparative advantage in the fixed rate market, while other companies have a comparative advantage inmarket, while other companies have a comparative advantage in floating rate market. Hence companies having comparativefloating rate market. Hence companies having comparative advantage in the fixed rate market might borrow fixed even thoughadvantage in the fixed rate market might borrow fixed even though even though it is desirous of a floating rate loan.Using a couponeven though it is desirous of a floating rate loan.Using a coupon swap, the company can convert fixed interest payments to floatingswap, the company can convert fixed interest payments to floating interest payments.interest payments. Benchmark interest ratesBenchmark interest rates Fixed -- yield on government bondsFixed -- yield on government bonds FLOTING -- LIBORFLOTING -- LIBOR Coupon swap results in reduction in borowing costs for both partiesCoupon swap results in reduction in borowing costs for both parties

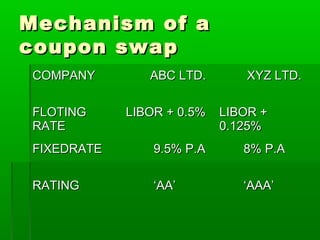

- 6. Mechanism of aMechanism of a coupon swapcoupon swap COMPANYCOMPANY ABC LTD.ABC LTD. XYZ LTD.XYZ LTD. FLOTINGFLOTING RATERATE LIBOR + 0.5%LIBOR + 0.5% LIBOR +LIBOR + 0.125%0.125% FIXEDRATEFIXEDRATE 9.5% P.A9.5% P.A 8% P.A8% P.A RATINGRATING ‘‘AA’AA’ ‘‘AAA’AAA’

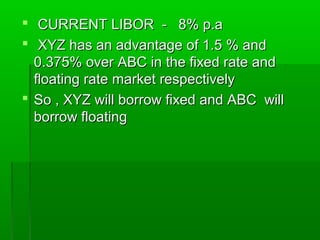

- 7. CURRENT LIBOR - 8% p.aCURRENT LIBOR - 8% p.a XYZ has an advantage of 1.5 % andXYZ has an advantage of 1.5 % and 0.375% over ABC in the fixed rate and0.375% over ABC in the fixed rate and floating rate market respectivelyfloating rate market respectively So , XYZ will borrow fixed and ABC willSo , XYZ will borrow fixed and ABC will borrow floatingborrow floating

- 8. Abc raises floating money pays 0.5% overAbc raises floating money pays 0.5% over libor to lenders receives libor from xyzlibor to lenders receives libor from xyz pays 8.5% fixed to xyzpays 8.5% fixed to xyz Xyz raises fixed rate pays 8% to lendersXyz raises fixed rate pays 8% to lenders pays libor to abc. Receives fixed 8.5%pays libor to abc. Receives fixed 8.5% from abcfrom abc

- 9. COSTCOST ABCABC XYZXYZ PRE- SWAP(A)PRE- SWAP(A) 9.5%9.5% LIBOR +LIBOR + 0.125%0.125% i.e.8.125i.e.8.125 POST-POST- SWAP(B)SWAP(B) 9%9% LIBOR - 0.5%LIBOR - 0.5% i.e 7.50%i.e 7.50% SAVINGS(A-B)SAVINGS(A-B) 0.5%0.5% 0.625%0.625%

- 10. TOTAL GAIN TO ALL PARTIES FROM THETOTAL GAIN TO ALL PARTIES FROM THE SWAPSWAP EQALS THE DIFFERENCE BETWEEN THEEQALS THE DIFFERENCE BETWEEN THE INTEREST RATES AVAILABLE FOR THEINTEREST RATES AVAILABLE FOR THE TWO COMPANIES IN THE FIXED MARKETSTWO COMPANIES IN THE FIXED MARKETS MINUS THE DIFFERENCE BETWEEN THEMINUS THE DIFFERENCE BETWEEN THE INTEREST RATES AVAILABLE TO THE TWOINTEREST RATES AVAILABLE TO THE TWO COMPANIES IN THE FLOATING RATE MKTSCOMPANIES IN THE FLOATING RATE MKTS I.E (9.50% - 8.0%) – (8.50% -8.125%)I.E (9.50% - 8.0%) – (8.50% -8.125%) =1.1250%=0.5% TO ABC =0.625% TO XYZ=1.1250%=0.5% TO ABC =0.625% TO XYZ

- 11. Coupon swap – a flowCoupon swap – a flow chartchart Abc requires 7 year fixed rate fundingAbc requires 7 year fixed rate funding Abc raises a 7 ear floating rate debt at 0.5%Abc raises a 7 ear floating rate debt at 0.5% over LIBOR9(i.e in the market where it has aover LIBOR9(i.e in the market where it has a comparative advantage,or a lowercomparative advantage,or a lower disadvantagedisadvantage Abc locates Xyz, a company which needs 7Abc locates Xyz, a company which needs 7 year floating rate funds(same amount andyear floating rate funds(same amount and parallel repayment), and has a comparativeparallel repayment), and has a comparative advantage over Abc in the fixed rate market.advantage over Abc in the fixed rate market.

- 12. Xyz raises a 7year fixed rate debt at 8%p.aXyz raises a 7year fixed rate debt at 8%p.a Xyz and Abc swap interest liabilities.XyzXyz and Abc swap interest liabilities.Xyz agrees to pay interest at say Libor to Abc , andagrees to pay interest at say Libor to Abc , and Abc agrees to pay interest at say 8.5% to Xyz.Abc agrees to pay interest at say 8.5% to Xyz. Xyz has now got floating rate funds at anXyz has now got floating rate funds at an effective cost of Libor to Abc but makes a profiteffective cost of Libor to Abc but makes a profit of 0.5% on the fixed side , or 0.625% belowof 0.5% on the fixed side , or 0.625% below what it would have otherwise paid for floatingwhat it would have otherwise paid for floating rate funds.rate funds.

- 13. Abc has now got fixed rate funds at anAbc has now got fixed rate funds at an effective cost of 9%p.a (it pays 8.55 toeffective cost of 9%p.a (it pays 8.55 to Xyz and makes a loss of 0.5% on theXyz and makes a loss of 0.5% on the floating side or below what it would havefloating side or below what it would have otherwise paid for fixed rate fundsotherwise paid for fixed rate funds

- 14. Swap constraintsSwap constraints I Counterparties should have differing andI Counterparties should have differing and mutually complementary needs.mutually complementary needs. II The principal amount borrowed by theII The principal amount borrowed by the counterparties should be of identical amountcounterparties should be of identical amount and maturity.and maturity. III Counterparty riskIII Counterparty risk -- in practice, major international banks step-- in practice, major international banks step in and run their own swap bookin and run their own swap book -- a bank would enter into a separate swap-- a bank would enter into a separate swap transaction with each partytransaction with each party

- 15. -- a bank would do a swap without the-- a bank would do a swap without the ready availability of a matchingready availability of a matching counterparty and hedge its exposures incounterparty and hedge its exposures in the market, until another counterpartythe market, until another counterparty with opposite requirement is located.with opposite requirement is located. -- Thus with an intermediary, the-- Thus with an intermediary, the comparative advantage gets slit threecomparative advantage gets slit three ways 9between the bank and the twoways 9between the bank and the two counterpartiescounterparties

- 16. Curency swapsCurency swaps 1. Exchange of cash flows1. Exchange of cash flows 2. On NPV basis, identical to covering on2. On NPV basis, identical to covering on forward basis.forward basis. 3. Optimise liability profile3. Optimise liability profile 4. Use as hedge against economic exposures4. Use as hedge against economic exposures 5. Timing – when temptation to do something5. Timing – when temptation to do something is leastis least 6. Accounting/tax implications6. Accounting/tax implications

- 17. Mechanics of aMechanics of a currency swapcurrency swap companycompany usdusd pdspds AA 6.5%6.5% 8.5%8.5% BB 8.5%8.5% 9.5%9.5% -- ‘ A’ has an advantage of 2% and 1% over ‘B’ in borrowing dollars and sterling respectively.

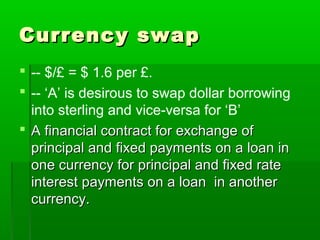

- 18. Currency swapCurrency swap -- $/£ = $ 1.6 per £. -- ‘A’ is desirous to swap dollar borrowing into sterling and vice-versa for ‘B’ A financial contract for exchange ofA financial contract for exchange of principal and fixed payments on a loan inprincipal and fixed payments on a loan in one currency for principal and fixed rateone currency for principal and fixed rate interest payments on a loan in anotherinterest payments on a loan in another currency.currency.

- 19. The exchange rate at which the principal andThe exchange rate at which the principal and interest payments are to be exchanged in theinterest payments are to be exchanged in the two currencies during the life of the swap is thetwo currencies during the life of the swap is the one ruling in the spot market on the day theone ruling in the spot market on the day the currency swap is entered into.currency swap is entered into. Like interest rate swaps , currency swaps areLike interest rate swaps , currency swaps are also motivated by comparative advantages.also motivated by comparative advantages. Currency swaps facilitate a corporate to alterCurrency swaps facilitate a corporate to alter its existing currency flows and risk:rewardits existing currency flows and risk:reward strategy.strategy.

- 20. Exchange of principal takes place at theExchange of principal takes place at the beginning and at the end whereasbeginning and at the end whereas interest payments occur during the life ofinterest payments occur during the life of the swap.the swap. usually banks act as intermediariesusually banks act as intermediaries thereby eliminating couterparty risk.thereby eliminating couterparty risk.

- 21. Basis swapBasis swap A swap in which a stream of floatingA swap in which a stream of floating interest rates are exchanged for anotherinterest rates are exchanged for another stream of floating interest rates is knownstream of floating interest rates is known as basis swap.Such type of swap isas basis swap.Such type of swap is possible when:possible when: Both the floating rate streams are based onBoth the floating rate streams are based on the same structure, but differentthe same structure, but different instruments.E:xample: a promise to payinstruments.E:xample: a promise to pay B and B promises to pay A 3 monthB and B promises to pay A 3 month LIBOR to 3 month treasury bill yield.LIBOR to 3 month treasury bill yield.

- 22. Interest base :money market9actual /360Interest base :money market9actual /360 or 365) or Bond (30 days month and 360or 365) or Bond (30 days month and 360 days year)days year) Periodicity annually, semiPeriodicity annually, semi annually,quarterlyannually,quarterly

Editor's Notes

- tation to do something is least